Foundry Outlook 2026-2027- Tariffs as the Macro Shock, Utilization as the KPI

Feb 01, 2026

Foundry Outlook 2026-2027: Tariffs as the Macro Shock, Utilization as the KPI

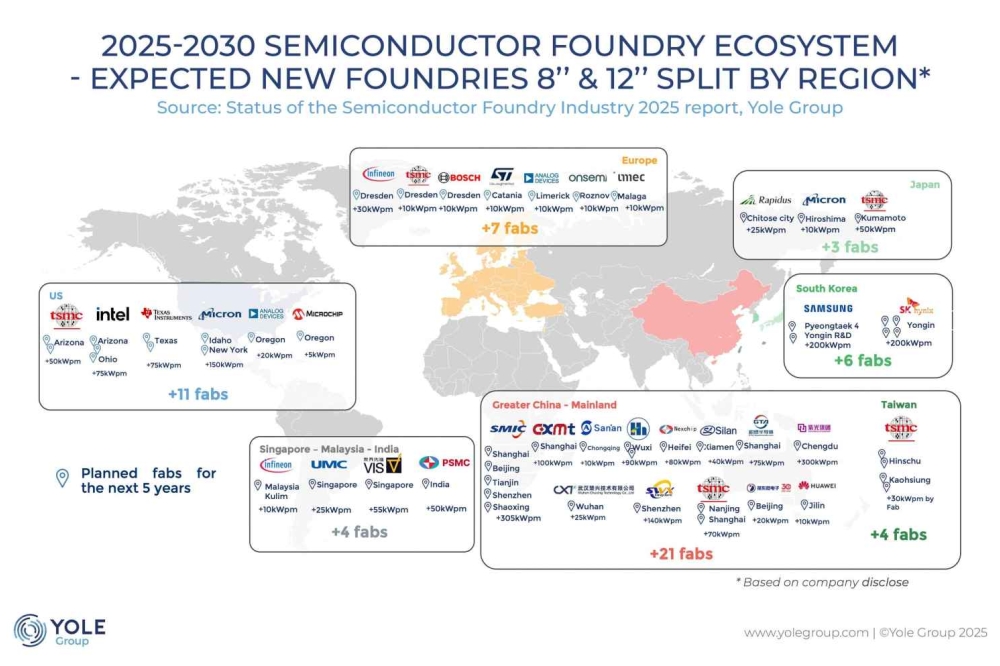

The wafer foundry industry is entering a new phase where policy shocks--especially 2025 U.S. tariffs--intersect directly with foundry economics. While the tariff environment is external, its consequences are internal: capacity placement, customer allocation, and long-term wafer agreements are now shaped by policy risk alongside cost and technology.

The wafer foundry industry is entering a new phase where policy shocks--especially 2025 U.S. tariffs--intersect directly with foundry economics. While the tariff environment is external, its consequences are internal: capacity placement, customer allocation, and long-term wafer agreements are now shaped by policy risk alongside cost and technology.

This article provides a neutral forecast for 2026 through 2027+, centered on foundry-specific metrics and decisions.

1) 2025 tariffs: the external variable that rewires internal decisions

Tariffs do not change transistor physics, but they do change contract structures and manufacturing footprints:

- Capacity location decisions now factor in tariff risk and origin rules, not just capex and labor.

- Customer allocation shifts toward multi-region sourcing to hedge policy exposure.

- Long-term wafer agreements (LTAs) become more common as customers lock in supply in tariff-resilient regions.

For foundries, the key question is no longer only "which node?" but also "which geography minimizes tariff and policy friction?"

2) Advanced nodes: demand is strong, utilization is the real story

AI and HPC demand continues to support leading-edge nodes in 2026, but foundry performance depends on how effectively capacity is utilized:

- Utilization rate becomes the most important operational KPI at advanced nodes.

- Yield ramp speed determines margin more than nominal pricing.

- Customer concentration increases: a small number of AI customers drive a large share of advanced-node wafers, raising revenue volatility.

Leading-edge foundries will likely prioritize longer LTAs and tighter co-development to reduce utilization swings.

3) Mature nodes: stable revenue base, strategic in tariffs

Mature-node volume remains the backbone of foundry revenue through 2026-2027:

- Automotive and industrial demand is steady and less cyclical than consumer electronics.

- Tariff pressure increases the appeal of local mature-node capacity.

- Utilization stability at mature nodes provides cash-flow predictability even when advanced-node demand is uneven.

Mature-node investments may expand in tariff-shielded regions, even if margins are lower.

4) Packaging: now a foundry differentiator, not an add-on

Advanced packaging has become a core element of foundry competitiveness:

- Packaging capacity constraints can bottleneck advanced-node revenue.

- Integrated offerings (wafer + package) improve gross margin and customer stickiness.

- Yield at package level increasingly determines end-to-end economics.

By 2027, packaging depth will likely be as decisive as lithography leadership.

5) 2026-2027 foundry strategy shifts

Foundry strategies are converging around a few patterns:

- Multi-region footprints to de-risk tariffs and export control surprises.

- Node portfolio balance to smooth utilization and revenue volatility.

- Pricing discipline tied to LTAs, with more volume locked under multi-year agreements.

- Co-design partnerships for advanced nodes to secure predictable demand.

These shifts reinforce an industry structure that rewards resilience as much as process leadership.

6) Watchlist: what matters most in 2026

For foundry-focused readers, these indicators will signal the market's direction:

- Utilization rates at leading-edge nodes

- Mature-node expansion plans outside Asia

- LTA coverage ratios for top foundries

- Packaging capacity announcements and lead-time changes

- Regional tariff or export-control adjustments affecting sourcing rules

These are the metrics that most directly translate policy changes into foundry outcomes.

7) Outlook beyond 2027

The most probable trajectory is a managed regionalization of capacity:

- Advanced nodes remain concentrated but more geographically diversified.

- Mature nodes become strategically distributed for tariff resilience.

- Packaging integration becomes the default in competitive bids.

In this environment, "best foundry" is no longer just a technology label--it is a combination of yield performance, utilization stability, and policy-resilient capacity.

Conclusion

The 2025 tariff environment is not a temporary headline; it is a structural signal. For foundries, it shifts decision-making toward regional diversification, tighter customer agreements, and a more integrated manufacturing-packaging model.

From 2026 through 2027+, the winners are likely to be foundries that balance advanced-node leadership with utilization discipline, mature-node stability, and a tariff-aware footprint strategy. Tariffs may be external, but their impact is now fully internal to foundry planning.